The Power of Zero-Based Budgeting: Spend Every Dollar Wisely

Zero-based budgeting is a strategic financial approach where every dollar of income is allocated to specific expenses, savings, or debt payments, ensuring no funds remain unassigned. This method enhances financial control by promoting intentional spending, minimizing waste, and boosting savings and debt repayment efforts. Although it requires regular tracking and adjustments, the discipline of zero-based budgeting can lead to significant financial improvements and adaptability to individual lifestyles.

Zero-based budgeting might sound like something straight out of a corporate boardroom, but it's actually a powerful tool for personal finance. At its core, zero-based budgeting is about giving every dollar a job. Whether it's paying bills, adding to savings, or tackling debt, each dollar you earn is purposefully assigned. This method can be a game-changer for anyone looking to take control of their finances, reduce wasteful spending, and boost their savings. It’s not just about tracking expenses—it's about intentional spending.

Imagine your income as a pie. Instead of leaving some slices unclaimed, zero-based budgeting ensures every piece is spoken for. It’s a proactive approach that encourages you to plan ahead, rather than react to bills as they come. While it might require more effort and diligence than a traditional budget, the benefits are well worth it. By regularly tracking your income and expenses, you can make informed decisions that align with your financial goals.

Understanding Zero-Based Budgeting

Zero-based budgeting flips the script on traditional budgeting. Instead of starting with last month's expenses, you begin with a clean slate each month. This means you’re not just assuming your spending will be the same as before; instead, you’re evaluating and justifying every expense from scratch. According to Dave Ramsey, a well-known personal finance guru, this approach forces you to be intentional with your money, which can lead to more mindful spending habits.

The process begins with listing all your income sources. Once you know how much money is coming in, you allocate it across various categories, including necessities like housing, utilities, and groceries, as well as savings and debt repayment. The aim is to make your income minus your expenses equal zero. If you find you've got extra cash, that's a signal to put those dollars to work—perhaps by bolstering your emergency fund or chipping away at a loan.

The Benefits of a Zero-Based Budget

One of the most significant advantages of zero-based budgeting is its ability to promote financial discipline. By assigning a purpose to every dollar, you're less likely to fritter away cash on impulse purchases. This budgeting style also enhances awareness of your spending habits, helping you identify areas where you might be overspending. For instance, you might realize that dining out consumes more of your budget than anticipated, prompting you to cut back and cook more at home.

Additionally, zero-based budgeting can boost your savings efforts. With clear allocations for savings goals, you’re more likely to meet them. Imagine setting aside a specific amount for a vacation fund each month—by the time you're ready to book a trip, you'll have the funds ready, avoiding the need to dip into savings or rack up credit card debt.

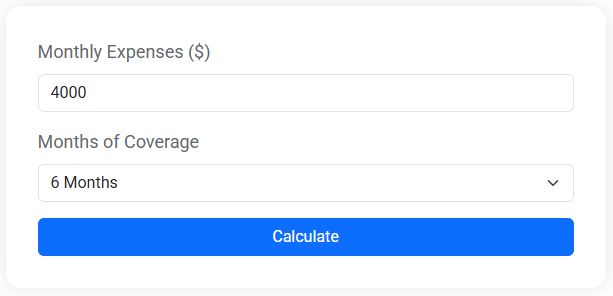

Emergency Fund Calculator

Wondering how much you should set aside for life's unexpected moments? Our Emergency Fund Calculator helps you quickly figure out how much you need to save to cover your expenses for 3, 6, or even 12 months. Whether you're building a financial safety net or planning for job loss, medical bills, or other emergencies, this tool gives you a clear savings goal to aim for — fast and easy.

Challenges and Considerations

While zero-based budgeting offers numerous benefits, it does require a commitment to regular tracking and adjustments. This level of detail can be daunting for some, especially if you're used to a more relaxed approach to budgeting. The key is consistency. Tools like budgeting apps or spreadsheets can make the process easier by automating tracking and providing insights into spending patterns.

Another consideration is the need for flexibility. Life is unpredictable, and expenses can arise unexpectedly. It's important to build a buffer into your budget for such events. As financial advisor Jane Smith explains, "Having a small emergency fund within your budget can prevent one-off expenses from derailing your financial plan."

Real-World Applications

Zero-based budgeting isn't just for individuals—businesses and governments use it too. But on a personal level, it can be adapted to fit any lifestyle. Take Sarah, a freelance graphic designer, for example. Her income fluctuates monthly, making traditional budgeting a challenge. By adopting a zero-based approach, she was able to prioritize essential expenses and savings, even during lean months. This method gave her the peace of mind that her financial bases were covered, regardless of her variable income.

Similarly, young families can benefit from zero-based budgeting. With childcare costs, groceries, and education expenses, it’s easy for spending to spiral. By budgeting from zero each month, families can ensure that their spending aligns with their priorities, such as saving for college or family vacations.

Getting Started with Zero-Based Budgeting

If you're ready to give zero-based budgeting a try, start by assessing your current financial situation. Gather information on your income and regular expenses. Next, set clear financial goals—whether it's building an emergency fund, paying off debt, or saving for a large purchase. Then, allocate your income to different categories, ensuring that every dollar is accounted for.

Remember, it's okay to make adjustments as you go. Life changes, and so should your budget. Regularly review your spending and tweak your allocations to better reflect your financial goals and lifestyle. As you become more comfortable with the process, you'll likely find that zero-based budgeting doesn't just improve your finances—it also reduces stress and increases your confidence in managing money.

Conclusion: The Long-Term Impact

Zero-based budgeting is more than just a financial strategy; it's a mindset shift. By making intentional decisions about where your money goes, you gain greater control over your financial future. This method encourages proactive planning, reduces unnecessary spending, and helps you achieve your financial goals faster. While it may require more effort upfront, the long-term benefits—financial stability, increased savings, and reduced debt—make it a worthwhile endeavor. Embrace the power of zero-based budgeting, and watch as your financial landscape transforms for the better.