Budgeting for Beginners: Simple Steps to Get Started

Budgeting, while initially intimidating, can become empowering by breaking it into manageable steps: understanding your income and expenses, setting clear financial goals, and creating a realistic budget plan. Consistently tracking spending and regularly adjusting your budget ensures it remains effective and aligned with your financial goals. By mastering these steps, you can take control of your finances, paving the way for financial stability and confidence.

Let's face it, the word "budgeting" often conjures images of endless spreadsheets and the slow, painful process of trimming the fun out of our lives. But what if I told you that budgeting doesn’t have to be a dreaded chore? In fact, it can be a surprisingly empowering tool that gives you a clear view of your finances and helps you achieve your dreams. Whether you're saving for a vacation, paying off debt, or just trying to make ends meet, a solid budget is your roadmap. And like any good map, it needs to be clear, easy to follow, and adaptable to changes along the way.

Many people think budgeting is about restriction. In reality, it's about understanding where your money is going, so you can make informed decisions that align with your priorities. It's a practice that can transform not just your bank account, but your overall peace of mind. So, if you're ready to take control of your financial future, let's break down the basics of budgeting into simple, manageable steps.

Understanding Your Income and Expenses

The first step to effective budgeting is getting a firm grasp on your cash flow. Start by taking a close look at your income. This might seem straightforward, but it's important to consider all sources. Are you relying solely on a paycheck, or do you have side gigs or freelance work adding to your coffers? Jot down your net income—what actually hits your bank account after taxes and deductions.

Next, dive into your expenses. Here’s where things can get a bit eye-opening. Track your spending for a month to understand your habits. You might be surprised to see how much those daily lattes add up over time. Categorize your expenses into fixed ones, like rent and utilities, and variable ones, such as groceries, dining out, or entertainment. This breakdown will help you identify areas where you have more control and where you might cut back if needed.

According to a 2022 survey by the Bureau of Economic Analysis, the average American household spends about $63,000 annually. Knowing where you stand relative to such benchmarks can offer a perspective on how typical your spending habits are, though personal goals and circumstances should always be the primary guide.

Setting Clear Financial Goals

Once you’ve got a handle on your income and expenses, it’s time to set some financial goals. Think of your budget as a tool to help you reach these goals, whether they're short-term, like saving for a new phone, or long-term, like buying a home. Goals give your budget purpose and direction, turning a static spreadsheet into a dynamic plan for your future.

Start by identifying what you want to achieve financially. Be specific. Instead of saying "I want to save money," say "I want to save $5,000 for a vacation next summer." This specificity provides you with a target to aim for and makes tracking progress much more straightforward.

Prioritize your goals based on urgency and importance. For instance, building an emergency fund might take precedence over funding a leisure activity if you currently have little to no savings. Remember, these priorities can change, so it's important to revisit them regularly.

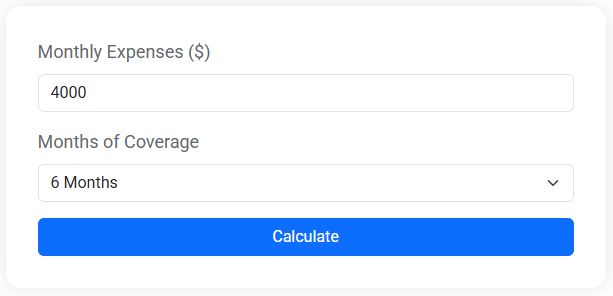

Emergency Fund Calculator

Wondering how much you should set aside for life's unexpected moments? Our Emergency Fund Calculator helps you quickly figure out how much you need to save to cover your expenses for 3, 6, or even 12 months. Whether you're building a financial safety net or planning for job loss, medical bills, or other emergencies, this tool gives you a clear savings goal to aim for — fast and easy.

Creating a Realistic Budget Plan

Armed with your financial goals, you’re ready to craft a budget. The aim here is to create a plan that’s realistic and sustainable—one that acknowledges your lifestyle while steering you toward your goals. Start by allocating your income toward different categories, using the information from your expense tracking.

A common guideline is the 50/30/20 rule, popularized by Senator Elizabeth Warren. It suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment. This framework is a great starting point, but feel free to adjust these percentages to better fit your personal situation.

Remember, a budget isn’t set in stone. Life happens, and your budget should be flexible enough to accommodate changes. Whether it's an unexpected car repair or a spontaneous dinner out, having a buffer in your budget can prevent these expenses from derailing your financial plans.

Consistently Tracking Spending

The key to sticking with a budget is regular tracking. This doesn’t mean obsessing over every penny, but rather maintaining a general awareness of your spending patterns. There are numerous apps, like Mint or YNAB (You Need A Budget), that can simplify this process by automatically categorizing transactions and providing real-time insights into your spending habits.

Set aside time each week to review your spending. Are you staying within your budgeted amounts, or are there areas where you're consistently overspending? This regular check-in helps you catch potential issues early and make adjustments before they become problems.

As financial advisor Jane Smith puts it, "A budget is like a garden; it requires regular tending to ensure that it grows in the direction you want." Regular tracking transforms your budget from a static document into a living tool that evolves with your financial life.

Regularly Adjusting Your Budget

Life is dynamic, and your budget should be, too. Regularly revisiting your budget helps ensure that it remains relevant and effective. Whether it's a change in income, a new financial goal, or an unexpected expense, revisiting your budget allows you to adapt to life's twists and turns.

Make it a habit to review your budget monthly or quarterly, depending on your comfort level. Look at what worked, what didn’t, and where you can make improvements. Perhaps you need to adjust your grocery budget or increase your savings allocation. These fine-tunings keep your budget aligned with your current reality and future aspirations.

According to a CNBC report, only 30% of Americans have a long-term financial plan including savings and investment goals, but those who do tend to feel more confident about their financial futures. By regularly adjusting your budget, you join this group of financially empowered individuals.

Mastering Budgeting: Taking Control of Your Finances

Budgeting may start as a necessity, but it evolves into a powerful tool for financial mastery. By understanding your income and expenses, setting clear goals, creating a flexible plan, and consistently tracking and adjusting your budget, you can take control of your financial life. This isn't just about saving money; it's about gaining confidence in your financial decisions and setting yourself up for a stable and successful future.

So, grab a cup of coffee, sit down with your financial details, and start building a budget that works for you. Remember, the ultimate goal is not perfection, but progress. With each thoughtful adjustment and each goal met, you’re taking steps toward a more financially secure and confident life.