Budgeting for Financial Independence: Steps to Achieve Your Goals

Achieving financial independence requires careful planning, disciplined budgeting, and setting clear financial goals. Start by assessing your current financial situation, creating a realistic budget, building an emergency fund, and investing wisely to grow your wealth. By remaining committed to these steps, you can work towards living life on your own terms and securing a financially independent future.

Achieving financial independence is a dream for many, but it’s not just about dreaming; it’s about planning. The concept of financial independence is all about having enough income to cover your living expenses without being reliant on a traditional job. It means having the freedom to pursue your passions without the constant pressure of financial worries. While it may sound daunting, reaching this level of freedom is entirely possible with deliberate budgeting and strategic financial planning.

The key to financial independence lies in breaking down the journey into actionable steps. It’s not about cutting out every luxury or living a monk-like existence. Instead, it’s about making informed choices that align with your long-term goals. In this article, we’ll explore practical steps to help you assess your financial situation, create an effective budget, build a safety net, and make your money work for you. Let's get started on the path to living life on your own terms.

Assessing Your Current Financial Situation

Before you can chart a course toward financial independence, it’s critical to understand where you currently stand. Gather all your financial documents, including bank statements, credit card bills, and investment accounts. This will give you a clear picture of your assets, debts, income, and expenses. Think of this as your financial health check-up.

Start by calculating your net worth, which is the difference between your total assets and liabilities. Knowing your net worth allows you to measure progress as you work towards your financial goals. For instance, if you have student loans, car payments, or credit card debt, these liabilities can significantly impact your financial journey. According to a 2023 report by Experian, the average American carries a credit card balance of over $5,000. Understanding how your debts affect your overall financial health is crucial in planning your path to independence.

Creating a Realistic Budget

Once you have a clear understanding of your financial standing, the next step is to create a budget that reflects your lifestyle and goals. A budget isn’t just a list of expenses; it’s a strategic plan for your money. Start by categorizing your expenses into needs and wants. Needs are non-negotiable expenses like housing, utilities, and groceries, while wants include dining out, entertainment, and hobbies.

A common budgeting model is the 50/30/20 rule, popularized by Senator Elizabeth Warren. This method suggests allocating 50% of your income to necessities, 30% to discretionary spending, and 20% to savings and debt repayment. However, feel free to adjust these percentages based on your individual circumstances. If you’re aiming for early retirement, you might lean more towards saving and investing. The goal is to create a budget that you can stick to, not one that feels restrictive.

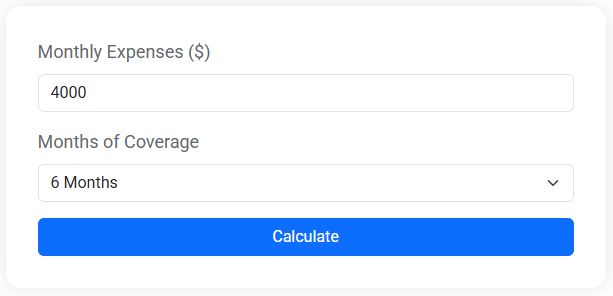

Emergency Fund Calculator

Wondering how much you should set aside for life's unexpected moments? Our Emergency Fund Calculator helps you quickly figure out how much you need to save to cover your expenses for 3, 6, or even 12 months. Whether you're building a financial safety net or planning for job loss, medical bills, or other emergencies, this tool gives you a clear savings goal to aim for — fast and easy.

Building an Emergency Fund

An emergency fund is your financial safety net, providing peace of mind when unexpected expenses arise. Whether it’s a car repair, medical bill, or sudden job loss, having a stash of cash to fall back on can prevent you from derailing your financial goals. Financial experts, including Suze Orman, recommend saving three to six months' worth of living expenses.

Start small if necessary; even $500 can cover minor emergencies and keep you from resorting to credit cards. Open a high-yield savings account to take advantage of compound interest while keeping your funds accessible. The key is consistency. Set up automatic transfers from your checking account to your emergency fund to gradually build a cushion over time.

Investing Wisely to Grow Your Wealth

Investing is a powerful tool for achieving financial independence, as it allows your money to work for you. The earlier you start investing, the more time your money has to grow. For those new to investing, the stock market may seem intimidating, but it’s one of the most effective ways to build wealth over time. Historically, the S&P 500 has averaged an annual return of about 10%, though past performance doesn’t guarantee future results.

Diversification is key to managing risk. Consider a mix of stocks, bonds, and index funds to spread your investments across various sectors and asset classes. If you're unsure where to start, a target-date retirement fund can be an excellent choice, as it automatically adjusts your asset allocation based on your retirement timeline. As Warren Buffett famously advises, "Do not put all your eggs in one basket."

Setting Clear Financial Goals

Financial independence requires clear, achievable goals. Without them, it's easy to lose motivation or get sidetracked. Define what financial independence means to you. Is it retiring early, traveling the world, or pursuing a passion project? Once you have a vision, break it down into smaller, actionable goals, such as paying off debt, increasing your savings rate, or reaching a specific investment milestone.

Use the SMART criteria—Specific, Measurable, Achievable, Relevant, Time-bound—to set effective goals. For example, instead of saying, "I want to save more," set a goal to "save $10,000 for a down payment on a house within the next two years." This approach provides clarity and direction, making it easier to track progress and celebrate achievements along the way.

Staying Committed to Your Plan

Achieving financial independence is a marathon, not a sprint. Staying committed to your budget and financial plan requires discipline and perseverance. Regularly review your progress and adjust your plan as needed. Life is full of changes, and your financial strategy should be flexible enough to adapt. Celebrate small victories to maintain motivation and remind yourself of the bigger picture.

Surround yourself with a supportive community, whether it’s a financial advisor, a group of like-minded friends, or online forums. Sharing experiences and learning from others can provide valuable insights and encouragement. Remember, setbacks are a natural part of the journey. The key is to stay resilient and focused on your ultimate goal of financial independence.

In conclusion, budgeting for financial independence is a journey that requires careful planning, disciplined saving, and smart investing. By assessing your current financial situation, creating a realistic budget, building an emergency fund, and investing wisely, you can work towards a future where you have the freedom to live life on your own terms. Stay committed, keep learning, and take control of your financial destiny.