Crush Your Debt: 7 Proven Strategies to Get Out Faster

Debt can feel overwhelming, but you're not alone, and there are effective strategies to tackle it. From using the snowball method to negotiating lower interest rates and increasing your income, these actionable steps—backed by expert advice—can help you regain financial freedom. By consolidating debt, automating payments, and seeking professional help if needed, you can take control of your financial future and reduce debt-related stress.

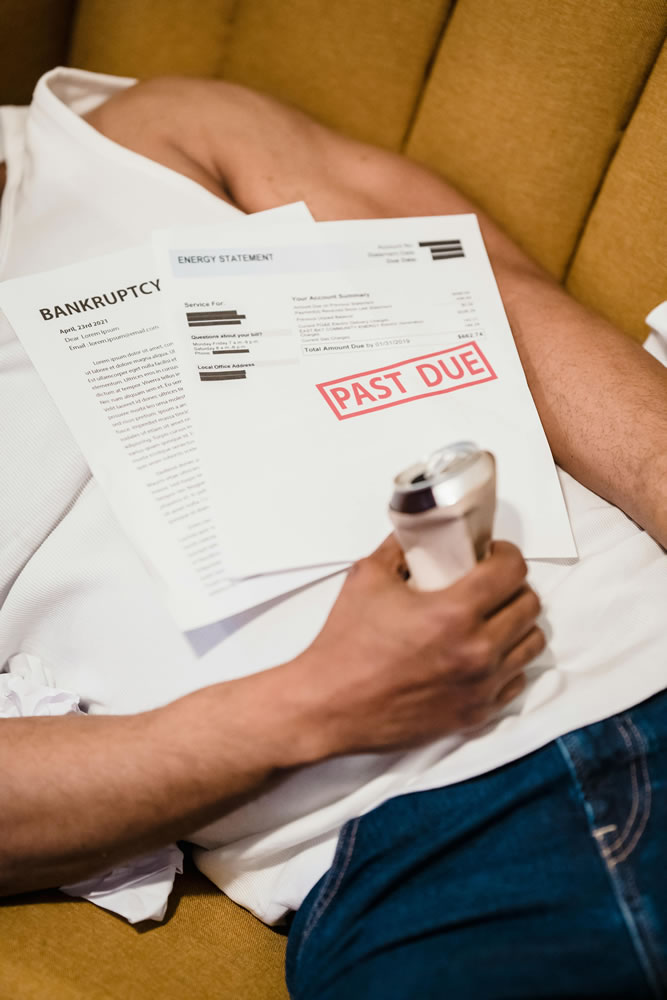

Debt. It’s a word that can make your stomach sink, your palms sweat, and your sleep restless. But here’s the thing: you’re not alone. Millions of people are navigating their way through the maze of loans, credit cards, and interest rates. The good news? There are tried-and-true strategies to help you crush your debt faster than you might think. Whether you’re dealing with student loans, lingering credit card balances, or a hefty mortgage, there’s hope and practical steps you can take to reclaim your financial freedom.

Let’s break down seven proven strategies to help you tackle debt effectively. These aren’t just theoretical tips; they’re actionable steps backed by experts and real-world success stories. Ready to transform your financial life? Let’s dive in.

1. Embrace the Snowball Method

The snowball method is a psychological powerhouse. Popularized by personal finance guru Dave Ramsey, this strategy focuses on paying off your smallest debts first while maintaining minimum payments on larger ones. The idea is simple: with each small victory, you build momentum and confidence. Imagine paying off a pesky $500 credit card balance. That win provides a psychological boost, making you more motivated to tackle the next debt.

Research shows that this method is effective because it taps into the power of small wins. According to a study by the Harvard Business Review, achieving minor goals can significantly boost your motivation and morale. So, list your debts from smallest to largest, and start knocking them out one by one. It’s like rolling a snowball downhill – once you get started, it picks up speed and power.

2. Cut Expenses and Redirect Savings

Budgeting might not be the most glamorous topic, but it’s essential. Take a hard look at your monthly expenses and identify areas where you can cut back. Maybe it’s the daily latte or that gym membership you rarely use. Every dollar saved is a dollar you can put toward your debt. According to CNBC, trimming just $100 a month from your budget can accelerate your debt payoff timeline significantly.

One practical approach is to use budgeting tools like Mint or YNAB (You Need A Budget) to track your spending. These apps can help you visualize where your money goes and make adjustments accordingly. The key is to redirect those savings into extra payments on your debt, hastening your journey to financial independence.

Debt Payoff Calculator

Plan your financial future by estimating how long it will take to pay off your debt based on your balance, annual percentage rate (APR), and monthly payment. After entering your figures, the calculator determines the number of months needed to fully repay the debt and calculates the total interest paid over time.

3. Negotiate Lower Interest Rates

Don’t underestimate the power of negotiation. If you’re dealing with credit card debt, calling your credit card issuer to request a lower interest rate can save you money and time. Many people are surprised at how amenable companies can be, especially if you’ve been a loyal customer. A lower interest rate reduces the total amount you’ll pay over time and allows more of your payment to go toward the principal balance.

Consider this: if you have a $5,000 balance with a 20% interest rate, reducing it to 15% could save you hundreds of dollars annually. According to a survey by CreditCards.com, about 70% of people who asked for a lower rate were successful. It might feel daunting, but picking up the phone can be a game-changer.

4. Increase Your Income

While cutting back on expenses is crucial, boosting your income can supercharge your debt payoff plan. Think about ways to earn more money, whether it’s through a side hustle, freelance work, or selling items you no longer need. Platforms like Fiverr, Upwork, or even local gigs can offer opportunities to earn extra cash.

Real-life example: Sarah, a teacher in Ohio, started tutoring students online and selling handmade crafts on Etsy. Within a year, she managed to pay off $10,000 in credit card debt. The additional income not only helped her tackle debt but also provided a sense of accomplishment and financial security. Increasing your income might require some hustle, but the results can be well worth the effort.

5. Consider Debt Consolidation

Debt consolidation can simplify your financial life. By combining multiple debts into a single payment, often with a lower interest rate, you can make your debt more manageable. Options include personal loans, balance transfer credit cards, or home equity loans. However, it’s crucial to do your homework and understand the terms before committing.

As financial advisor Jane Smith explains, “Debt consolidation can be a smart move if it reduces your interest rate and helps you pay off debt faster. But it’s not a one-size-fits-all solution. Make sure the math works in your favor.” By consolidating debt, you can streamline payments and potentially save money, but always read the fine print and consider any fees involved.

6. Automate Your Payments

Out of sight, out of mind – that’s the beauty of automation. Setting up automatic payments ensures you never miss a due date, avoiding late fees and additional interest charges. Most banks and lenders offer this feature, allowing you to pay a fixed amount toward your debt each month without lifting a finger.

Automation creates consistency in your financial routine, helping you stay on track even during busy or stressful times. Plus, seeing your debt shrink with each automatic payment can be incredibly satisfying. It’s like setting your finances on autopilot and watching the results unfold.

7. Seek Professional Help if Needed

Sometimes, tackling debt can feel overwhelming, and that’s okay. If you’re struggling to manage on your own, seeking help from a certified credit counselor can be a wise investment. Non-profit organizations like the National Foundation for Credit Counseling (NFCC) offer resources and guidance to help you create a customized debt repayment plan.

According to a report by the NFCC, individuals who engage with credit counseling often develop better financial habits and experience improved credit scores. A professional can offer a fresh perspective, negotiate with creditors on your behalf, and provide support as you work toward financial freedom. Remember, asking for help is a sign of strength, not weakness.

Debt doesn’t have to be a life sentence. By applying these strategies, you can take control of your financial future and reduce the stress that debt brings. It won’t happen overnight, but with persistence and a plan, you’ll be amazed at what you can achieve. So, pick a strategy or two that resonates with you and start making progress today. Your future self will thank you.